Greece is on the verge of a third economic megacycle irrespective of who wins the elections, Barclays Bank analysts forecast.

The British multinational published a big report on Greece earlier in the week lauding the economic performance of Greece, which has been “transformed from an economic basket case to European growth tiger,” as the Financial Times notes.

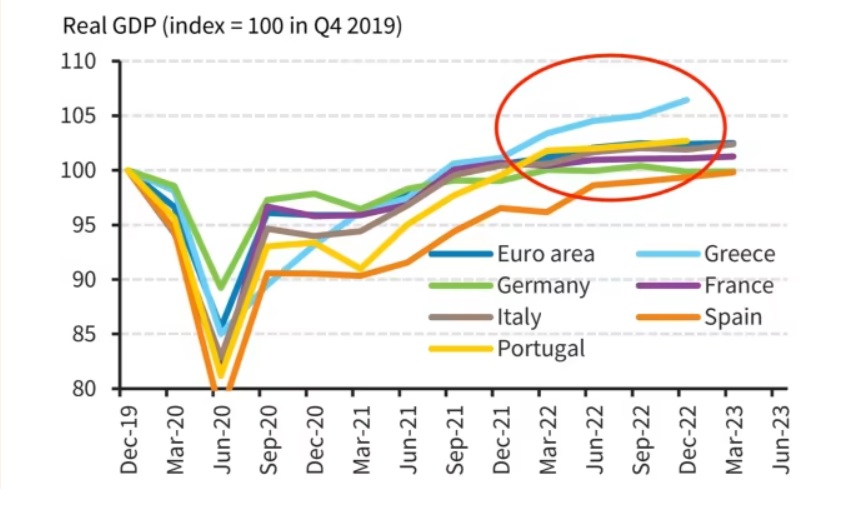

The publication of the report by Barclays coincided with the European Commission’s spring 2023 economic forecasts that revised forecasts for growth in Greece upwards.

Greece’s growth is expected to be “double the eurozone average” in 2023, at 2.4%, the European Commissioner for Economy, Paolo Gentiloni, said on Monday.

“Overall I think the results are very positive, we have a forecast of 2.4% growth this year, which is twice the eurozone average, and of course, we will see how things go next year,” the Commissioner said, adding: “It is difficult for me to highlight the negative elements when we have a lot of positive elements.”

Greece’s economic history has been marked by two megacycles

Barclays says Greece is not a typical economy that goes through 7-8 year cycles. Instead, its post-WW2 economic history has been marked by two megacycles, deeply linked to structural forces and political choices.

The first megacycle took place between the 1950s and the mid-1970s.

“The arrival of foreign aid — mainly as a result of the Marshall Plan — coupled with protectionist industrial and foreign exchange policies, as well as foreign economic supervision, produced an economic miracle: Greece, albeit from a low base, posted years of growth rates seen mainly in rapid growth emerging economies of the time such as South Korea,” Barclays says.

This first megacycle was followed by a protracted slump in activity, which lasted until the early 90s. Despite improved living conditions, politics were exceptionally unstable and democratic institutions frail.

“The lifting of industrial policies and protectionism (coupled with global oil and inflation shocks) led to a process widely known as ‘premature de-industrialization’,” the report notes.

This period laid the ground for Greece’s second megacycle. The arrival of structural funds from the EU, depreciation of the drachma, deep infrastructure investment, and convergence policies soon led to the resumption of growth.

“Starting intermittently from the mid-80s but accelerating in earnest after the signing of the Maastricht Treaty in 1992, the Greek economy had grown more than five-fold as a share of the German economy by 2008.

“At the end of this second megacycle, Greece had built substantial imbalances. Reliant on increasing amounts of government borrowing and external funding, operating at an uncompetitive cost level and consuming an unreasonable share of potential income, the economy was setting itself up for the 2010-2019 collapse,” Barclays says.

A potential third megacycle for Greece

Today, Greece has the opportunity for a third megacycle given three key dynamics, the Barclays report forecasts and explains:

1. Global services are becoming more tradeable, giving Greece a good chance to build an internationally competitive sector for the first time in its post-war history. Specifically, global trade in services are increasingly tradeable and are outperforming goods in terms of global trade growth.

2. This trend accelerated during the years of the Greek crisis and Greece is now catching up to it. Services constitute a good 75-80% of the GDP of Greece. Greece is hence much more likely to be competitive in its areas of comparative advantage (tourism, real estate, transportation, IT, clean energy, healthcare) than to build a new auto manufacturing industry.

3. The issues facing Europe as a whole (energy security, energy transition, protectionism from China and the US) are reducing the focus on intra-European budget frictions and introducing a new focus on cross-EU policies set to address the challenges ahead.

4. Greece is starting from a low level of activity (a large output gap), with many fewer imbalances than in the past, benefiting from structural reforms and infrastructure investment and in receipt of NGEU funds, which in their current form will be levered to reach up to €60bn — which is extremely large in the context of the size of the Greek economy (c.€200bn).

Can Greece capitalize on these dynamics?

Can Greece capitalize on these dynamics, given its many institutional and cost disadvantages, Barclays ponders?

Foreign Direct Investment in both manufacturing and services has spiked in the last two years. There is clearly a sense that Greece is directly investable to a greater extent than in the recent past, and certain big deals in the technology and payments sector are pointing that way, the report says.

In consequence, there seems to be more than just COVID-related growth base effects in Greece’s rapid post-pandemic recovery. Sustaining this momentum will be key to entering yet another multi-year high-growth megacycle.

“The incumbent government should also be credited for this surge in investment — market confidence is a sign of investor-friendly policies.

“It is thus no accident that many rating agencies are waiting for the election result and its implications for political stability and reform momentum before a critical potential upgrade to investment grade,” the Barclays report says.

See all the latest news from Greece and the world at Greekreporter.com. Contact our newsroom to report an update or send your story, photos and videos. Follow GR on Google News and subscribe here to our daily email!